How to Build a Dividend Portfolio That Generates $1,000 Monthly Income

Many investors in the US and Europe dream of covering their rent, groceries, or utility bills with stable dividend income. Building a portfolio that targets around 1,000 dollars or euros per month is achievable for disciplined, long‑term investors who follow a structured plan rather than chasing the highest yield.

- $1,000 in monthly income means $12,000 in annual dividends, which is the real planning target.

- The capital you need depends mainly on your average dividend yield and tax situation, not on a single "magic" stock.

- Diversified portfolios of quality dividend stocks and ETFs tend to be more resilient than concentrated bets on ultra‑high‑yield names.

- Reinvesting dividends and adding regular contributions can significantly shorten the time needed to reach your income goal.

Step 1: Understand What Dividend Income Really Is

A dividend is a cash payment that a company or fund distributes to its shareholders, usually every quarter in the US and frequently quarterly or semi‑annually in Europe. It is typically funded from the company's profits and reflects the board's confidence in the sustainability of its business model over time.

The most important concept for planning income is the dividend yield, which is the annual dividend per share divided by the current share price. If a stock trades at 50 and pays 2 per share every year, its yield is 4 percent. Yield changes when the share price moves or when the company adjusts its dividend policy.

Step 2: Translate $1,000 Per Month into Required Capital

To design a portfolio, convert your monthly goal into an annual target and relate it to your expected average dividend yield. A goal of $1,000 per month corresponds to $12,000 per year in dividends. The required capital is the annual income divided by the expected yield expressed as a decimal.

The table below shows how much capital would be needed at different average yields to target $12,000 in annual dividends. These figures are purely illustrative and do not represent any specific product or guarantee of returns.

| Average portfolio dividend yield | Annual income target | Approximate capital required |

|---|---|---|

| 2% | $12,000 | $600,000 |

| 3% | $12,000 | $400,000 |

| 4% | $12,000 | $300,000 |

| 5% | $12,000 | $240,000 |

| 6% | $12,000 | $200,000 |

Most long‑term investors aim for a balanced range, often around 3 to 5 percent, rather than extremely high yields that may be unsustainable. When thinking in euros instead of dollars, the logic is exactly the same; only the currency symbol changes.

Step 3: Consider Taxes and Location (US vs Europe)

Dividend taxation varies significantly between countries, and even within Europe there are major differences between, for example, Germany, France, and the Nordic markets. In the US, qualified dividends often receive a preferential rate compared with regular income, while some European investors pay a flat withholding rate plus possible local surcharges.

If you buy foreign stocks or ETFs, there can also be withholding taxes at the source country before the dividend even reaches your account. Many investors in Europe who own US stocks, for instance, will see a standard withholding applied that may or may not be partially reclaimable depending on local tax treaties. Because of these complexities, serious income investors almost always coordinate their strategy with a tax adviser in their jurisdiction.

Step 4: Choose Your Dividend Building Blocks

A robust dividend portfolio usually combines several types of income‑producing assets. No single category is perfect; each has trade‑offs in terms of volatility, yield level, and diversification. The table below summarizes some of the most common building blocks used by US and European investors.

| Asset type | Typical characteristics | Role in portfolio |

|---|---|---|

| Blue‑chip dividend stocks | Established companies with long records of paying and often raising dividends; moderate yields. | Core holdings for stability and gradual dividend growth. |

| Dividend growth stocks | Companies that start with moderate yields but increase payouts regularly as earnings grow. | Protect purchasing power against inflation over long horizons. |

| High‑yield stocks and REITs | Higher starting yields but often more sensitive to interest rates, leverage, or sector cycles. | Boost current income but require strict diversification and risk control. |

| Dividend ETFs | Funds that hold baskets of dividend‑paying stocks in the US, Europe, or globally. | Instant diversification and convenient way to access many companies at once. |

| Preferred shares and income funds | Hybrid securities that can offer relatively high yields with bond‑like features. | Additional income layer, especially for investors comfortable analyzing credit risk. |

When constructing your own mix, think in terms of a spectrum: some holdings prioritize safety and dividend reliability, others offer higher income but require closer monitoring. The exact balance depends on your risk tolerance, age, and how dependent you are on dividends for everyday expenses.

Step 5: Design a Sample Allocation to Target $1,000 Monthly

The following example shows how a diversified dividend portfolio might look for an investor targeting $1,000 in monthly income. The assumed yields are purely illustrative, designed to demonstrate the logic of mixing different assets rather than to recommend any specific security.

| Portfolio component | Allocation | Illustrative yield | Annual income per $300,000 invested |

|---|---|---|---|

| Global dividend ETF (US + Europe) | 40% | 3.0% | $3,600 |

| Blue‑chip dividend stocks | 30% | 3.5% | $3,150 |

| REITs and infrastructure | 20% | 5.0% | $3,000 |

| Preferreds and income funds | 10% | 5.5% | $1,650 |

| Total | 100% | Weighted ≈ 3.9% | $11,400 |

In this simplified illustration, a $300,000 portfolio with a weighted yield close to 4 percent would produce around $11,400 in annual dividends, which is just under the $12,000 target. Increasing the capital slightly, raising the average yield by carefully adding quality high‑income positions, or reinvesting dividends for a few years could close that remaining gap.

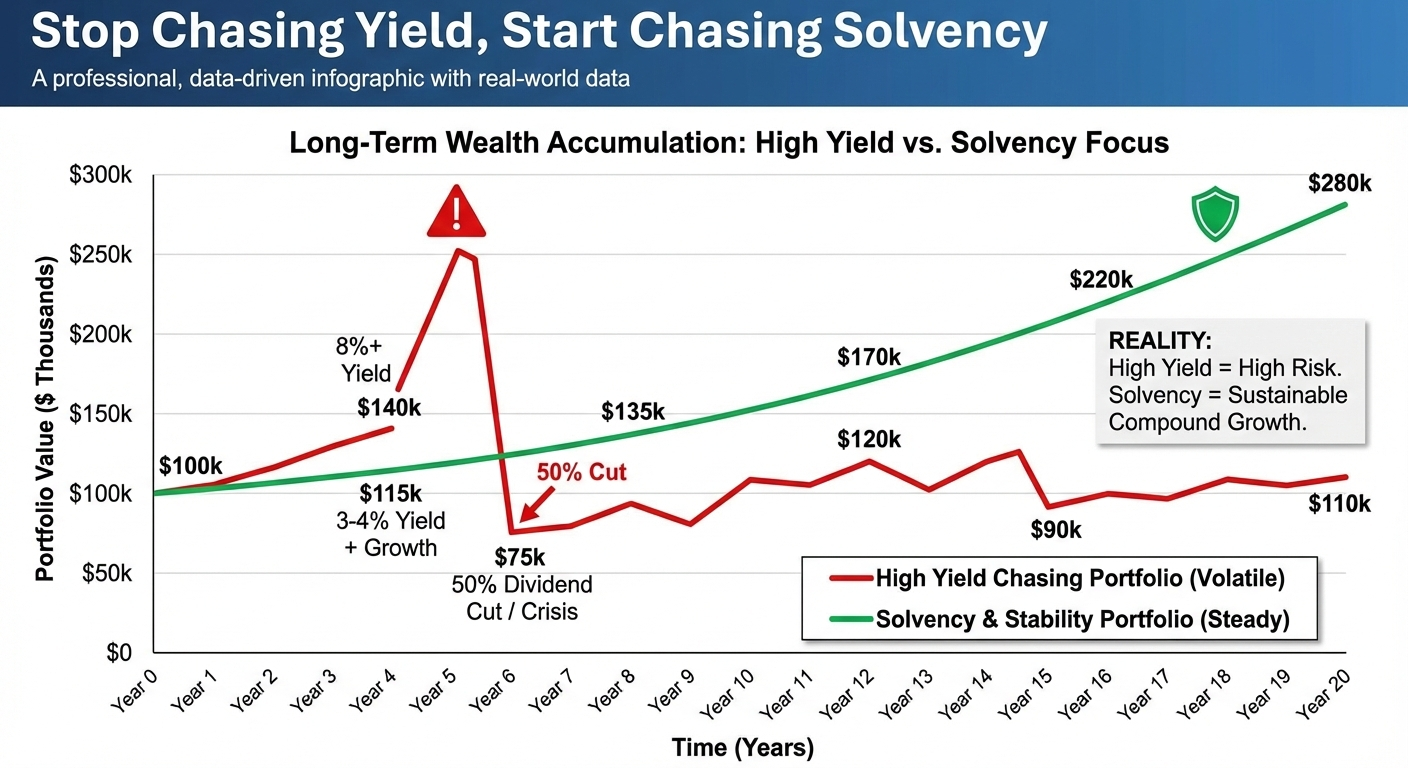

Step 6: Visualize How Yield Affects Required Capital

Many investors underestimate how powerful even a one‑percentage‑point change in average yield can be when applied to large portfolios. The chart below uses the same hypothetical $12,000 annual income target and shows approximate capital requirements at different yield levels.

This simple visualization highlights why chasing very high yields is risky. A portfolio yielding 6 percent reduces the capital needed, but those yields often come with concentrated sector exposure, leverage, or companies whose dividends may be vulnerable in a downturn. Many investors prefer accepting a higher capital requirement in exchange for better quality and sustainability.

Step 7: Diversify Across Sectors, Regions, and Payout Schedules

For investors in both North America and Europe, diversification is not only about owning many companies; it is also about reducing dependence on a single country, currency, or industry. Combining US and European dividend payers can spread political, regulatory, and interest‑rate risks, although it also introduces currency fluctuations that should be monitored.

Another practical tactic is to mix holdings with different payout months and frequencies. Some companies pay dividends in January, April, July, and October, while others choose different quarters; a few funds even pay monthly. Carefully arranging these patterns can smooth out your cash‑flow profile so that your income stream better matches your recurring expenses.

Step 8: Focus on Quality Metrics, Not Just Yield

The most dangerous mistake in dividend investing is filtering stocks only by current yield. A very high yield can signal that the market expects trouble, such as declining earnings, excessive debt, or an unsustainable payout ratio. Responsible income investors dig into the company's financial statements and track record before committing capital.

Key quality indicators to check

- Payout ratio relative to earnings or free cash flow.

- History of maintaining or growing dividends through past recessions.

- Stable or rising revenue and profit trends over several years.

- Reasonable debt levels and interest coverage.

- Competitive advantages such as strong brands or network effects.

Red flags that may warn of cuts

- Dramatic price drops not explained by broad market moves.

- Very high payout ratios combined with shrinking earnings.

- Frequent share issuances to finance the dividend.

- Sector disruptions (for example, sudden changes in regulation or technology).

- Management guidance that hints at cash‑flow pressure.

Many modern stock‑analysis platforms make it easier to screen for these metrics in both US and European markets, helping investors identify companies whose dividends are backed by solid fundamentals rather than fragile promises.

Step 9: Use Contributions and Reinvestment to Reach Your Goal Faster

Not every investor starts with $300,000 or more in available capital. The good news is that regular contributions and dividend reinvestment can steadily grow both your portfolio size and your future income. Even modest monthly investments can compound significantly over a decade or longer if combined with a disciplined strategy.

One common approach is to reinvest all dividends while you are still in the accumulation phase, using the cash to buy additional shares of your strongest positions or to diversify into new ones. Once your portfolio is large enough and your life situation requires it, you can gradually transition from automatic reinvestment to taking a portion of your dividends in cash.

Step 10: Manage Risks and Set Realistic Expectations

Even the most carefully designed dividend portfolio is exposed to market cycles, interest‑rate moves, and company‑specific shocks. Stock prices can fall sharply during recessions, and some businesses will inevitably cut or suspend dividends at some point. Planning only for ideal scenarios can leave income investors vulnerable when conditions change.

Sensible risk management includes holding an emergency cash buffer outside the portfolio, avoiding concentration in a single sector such as banks or energy, and staying flexible about temporarily accepting a lower income than 1,000 per month if that allows you to protect capital during severe downturns. It is better to pause withdrawals than to be forced into selling quality assets at depressed prices.

Practical Checklist Before You Invest

Before committing serious money to a dividend strategy, work through the following checklist. It will help align your expectations with reality and reduce emotional decision‑making when markets become volatile.

- Define clearly whether the $1,000 monthly goal is before or after taxes and fees.

- Estimate your time horizon and how much capital you can add each month or year.

- Map out a target allocation across ETFs, stocks, REITs, and other income assets.

- Verify quality metrics for each holding, including payout ratios and debt levels.

- Check tax rules and potential withholding for foreign dividends in your country.

- Decide which portion of dividends will be reinvested and for how long.

- Set rules for reviewing your portfolio, for example once per quarter.

- Document your plan so you can refer to it when headlines become stressful.

Final Thoughts

Building a dividend portfolio that aims to generate $1,000 per month is a long‑term project, not a weekend experiment. The core ingredients are realistic expectations, patience, diversification across high‑quality income assets, and consistent contributions during your working years.

Instead of searching for a single high‑yield stock that promises quick riches, focus on constructing a resilient collection of companies and funds that collectively deliver sustainable cash flow. Over time, this disciplined approach can turn volatility into opportunity and transform market corrections into moments to buy future income at better prices.