Market swings in both the United States and Europe have reminded investors that volatility is not an abstract concept — it is a lived experience that can shake even the most confident saver. Dollar-cost averaging (DCA) has become one of the most widely discussed strategies for building long-term wealth while reducing both financial and emotional risk, and the research behind it is richer than most investors realise.

📌 What Dollar-Cost Averaging Actually Is

Dollar-cost averaging means investing a fixed amount of money at regular intervals — weekly, monthly, or quarterly — regardless of whether markets are rising or falling. Instead of trying to guess the perfect entry point, you commit to a schedule and let prices dictate how many units you buy each time.

When prices are high, your fixed contribution buys fewer shares. When prices are low, it buys more — which gradually lowers your average cost per share over time. This mechanical approach removes the pressure to "time the market" and turns investing into a repeatable habit rather than a series of stressful, one-off decisions.

- You invest based on the calendar, not the news cycle or market sentiment.

- The same monthly contribution buys more units during downturns and fewer during bull runs.

- Your average cost per share smooths out naturally across full market cycles.

- Emotional investing errors — panic selling and FOMO buying — are structurally reduced.

- It works inside any account: 401(k), IRA, ISA, or a standard brokerage account.

📊 The Research in Numbers

🌍 Why DCA Matters for U.S. and European Investors

In the United States, the most common form of DCA is the automatic payroll contribution into 401(k)s and IRAs, where workers invest a slice of every paycheck into diversified mutual funds or ETFs — often with an employer match that amplifies the long-term result.

Across Europe, identical patterns appear in monthly ETF savings plans offered by brokers in Germany, France, the Netherlands, and the Nordics, where investors set a fixed euro amount into global or regional index funds each month. Regular contributions align naturally with how most people receive income — as monthly salaries — making DCA the single most practical investing strategy on both sides of the Atlantic.

401(k) auto-contributions, Roth IRA monthly investing, low-cost index fund platforms like Vanguard, Fidelity, and Schwab all natively support DCA at near-zero cost.

ETF savings plans via brokers like Trade Republic, Scalable Capital, and Degiro let investors set monthly investments from as little as €10 into MSCI World or Euro Stoxx index funds.

🔬 What Major Studies Found: DCA vs. Lump-Sum

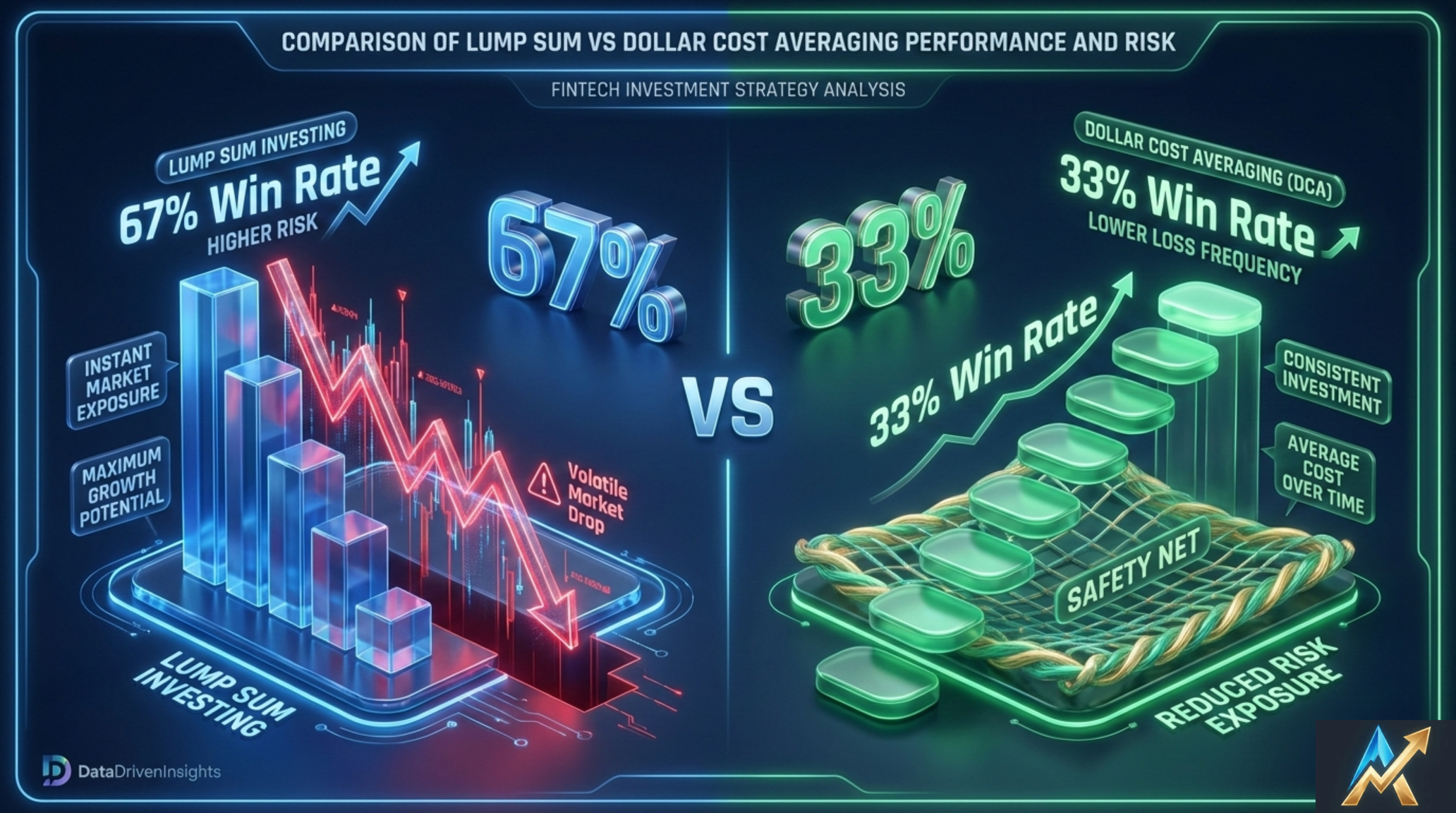

Three landmark studies from Vanguard, Morningstar, and Morgan Stanley have examined DCA versus lump-sum investing across different markets, time periods, and portfolio constructions. Their combined findings paint a nuanced but consistent picture.

| Study | Markets & Period | Key Finding | Where DCA Wins |

|---|---|---|---|

| Vanguard Research | U.S., U.K., Australia 1926–2011 |

Lump-sum beat 12-month DCA in ~67% of rolling 10-year periods across all three markets. | Lower loss frequency DCA lost money only 17.6% of the time vs. 22.4% for lump-sum. |

| Morningstar Analysis | 60/40 & all-equity portfolios Multiple historical periods |

Lump sum outperformed in roughly two-thirds of modelled scenarios; DCA won in about one-third. | Bear market protection DCA consistently outperformed in sharp, prolonged downturns. |

| Morgan Stanley WM | Historical & simulated portfolios Seven-year horizons |

Lump-sum generated higher annualised returns in >56% of historical cases when DCA was spread over 3+ months. | High volatility environments DCA delivered better risk-adjusted outcomes when expected returns were low and volatility high. |

📈 Visualising the Trade-Offs

The chart below presents two views side by side: how often each strategy outperformed across the three major studies, and the loss frequency comparison from Vanguard's dataset — arguably the most important figure for real-world investors.

🐻 How DCA Reduces Risk in a Bear Market

An American Century analysis modelled what happens when an investor enters a declining market: one investor commits the full six months of contributions on day one (lump sum); the other spreads the same total amount across six equal monthly contributions (DCA). The results are striking.

For most investors, avoiding a severe early loss matters more than maximising every last basis point of return — because a painful early experience can cause them to abandon their entire plan at the worst possible moment. DCA reduces this "regret risk" structurally, by ensuring that later contributions always benefit from lower prices during drawdowns.

⚡ Fresh Evidence from Recent Market Volatility

The turbulence of the early 2020s — the pandemic crash of March 2020, surging inflation through 2022, and rapid interest-rate hikes by the Fed and ECB — gave investors a real-time laboratory for stress-testing their approaches. DCA investors who stayed the course through the S&P 500's 34% plunge in March 2020 and continued buying during the trough were significantly better positioned for the recovery that followed over the next 12 months.

A 2026 guide from Saxo Bank illustrates a clear modern example: an investor choosing between a $12,000 lump sum or 12 monthly contributions of $1,000 into a volatile stock. By steadily buying more shares during dips, the DCA investor accumulates 125 shares with an average cost of $96, versus 120 shares at $100 for the lump-sum investor — a meaningful advantage in both quantity and unit cost before any market recovery even begins.

🛠️ How to Implement a DCA Strategy: Step by Step

The most effective DCA plans are simple enough to run entirely on autopilot once they are set up. The key is to make as many decisions as possible in advance, so that you have nothing to react to when markets get uncomfortable.

- Define your target portfolio. Choose a globally diversified mix — typically equity index funds covering the S&P 500, MSCI World, or STOXX Europe 600, potentially combined with bonds depending on your time horizon and risk tolerance.

- Set your fixed contribution amount. Choose a sum you can comfortably maintain in both good times and bad — the number should not require you to cut essential spending even during a recession.

- Automate the transfer. Link contributions to your pay cycle: auto-deduction into a 401(k) for U.S. workers, or a monthly standing order into an ETF savings plan for European investors.

- Select a tax-advantaged wrapper. Use IRAs, 401(k)s, ISAs, or European pension accounts to shelter dividends and gains from annual taxation, amplifying long-run compounding.

- Set a rebalancing schedule — not a panic trigger. Review allocation once or twice a year based on your long-term plan, not in response to market headlines.

- Stay the course. The single biggest DCA risk is pausing contributions during downturns — exactly when the strategy is working hardest in your favour by buying more units at lower prices.

🏗️ Choosing the Right Assets for DCA

Dollar-cost averaging works best with broadly diversified, growth-oriented assets whose long-term trend is upward — even if the path is volatile. Single stocks, narrow sector funds, or speculative assets introduce concentration risk that DCA cannot eliminate, since the strategy only helps with entry timing, not with diversification itself.

| Asset Type | DCA Suitability | Why |

|---|---|---|

| Global equity index funds (S&P 500, MSCI World) | Excellent | Diversified, long-term upward trend, low cost, liquid |

| European index funds (STOXX 600, Euro Stoxx 50) | Excellent | Regional diversification, EUR-denominated, tax-efficient in Europe |

| Dividend ETFs | Very Good | Reinvested dividends amplify compounding over time |

| Bond funds (investment grade) | Good (lower risk) | Smooths volatility, especially as you approach retirement |

| Individual stocks | Caution | Concentration risk — DCA doesn't protect against single-company failure |

⚠️ When DCA May Not Be the Best Choice

If you have received a large windfall — an inheritance, a bonus, or proceeds from a property sale — that you will not need for many years, and you are comfortable with short-term volatility, the statistical weight of evidence suggests investing it as a lump sum is more likely to maximise your long-run outcome. This conclusion holds across U.S., U.K., and Australian markets in the Vanguard dataset, as well as in Morningstar's and Morgan Stanley's independent analyses.

DCA can also lose its cost advantage when transaction fees are high, since frequent small purchases accumulate more trading costs than a handful of larger trades. This is less of a problem today with zero-commission brokers, but remains relevant on some European platforms with per-trade fees. The solution is simple: choose a platform with flat monthly or zero fees on ETF savings plans before implementing DCA.

🔀 Blending DCA with Lump-Sum Investing

Many experienced investors combine both approaches rather than choosing one exclusively. A practical framework: use DCA for all regular income-based savings (monthly salary contributions), and deploy unexpected large sums such as bonuses or inheritances as either an immediate lump sum or split across three to four monthly tranches — capturing most of the time-in-market advantage while reducing regret risk if markets happen to fall immediately after.

The key is to decide the rule in advance and commit to it, rather than improvising based on how confident you feel about the market on any given week. Most investing mistakes are made not through bad strategy selection, but through strategy abandonment at exactly the wrong moment.

🎯 Building a Resilient Portfolio with DCA

For U.S. and European investors building long-term wealth, dollar-cost averaging offers a disciplined framework that turns saving into an automatic habit and helps you remain invested through the turbulent periods that periodically test every investor's resolve. The evidence is clear that you may give up some expected return versus an immediate lump-sum — but you are statistically likely to experience fewer and shallower drawdowns, which for most human beings is the difference between staying the course for 30 years and abandoning the plan during the first serious market correction.

The most important question is not which strategy wins the most backtests, but which strategy you can genuinely live with across decades of market cycles, life changes, and economic uncertainty. By pairing consistent monthly contributions with globally diversified, low-cost index funds inside a tax-advantaged account, dollar-cost averaging gives every investor — regardless of income level or market knowledge — a realistic path to long-run financial resilience.

📚 Further Tools & Resources

Analyse individual stocks, explore portfolio strategies, and access professional-grade financial tools at ApexTicker.